In Tracking Home Ownership, Marriage Matters

Home ownership has long been considered a key metric for economic well-being in the United States. Thus many are dismayed by the fact that at 63.5 percent, the 2015 overall home-ownership rate appears to be lower than the 64.3 percent of 1985, a generation ago. But viewed in another, arguably more relevant way, the underlying trend shows that the home-ownership rate is, in fact, increasing, not decreasing.

How so? Key to the trend is the extremely strong relationship between marriage and home ownership — a relationship seldom, if ever, addressed in housing finance discussions. But if you think about it, it’s obvious that home ownership should be higher among married couples than among other households; in fact, it’s remarkably higher.

This relationship holds across all demographic groups. Importantly, it means that changes in the proportion of married vs. not-married households is a major driver of changes in the overall home-ownership rate over time. Home ownership comparisons among demographic groups are similarly influenced by differences in their respective proportions of married vs. not-married households.

Policy discussions over falling home-ownership rates frequently ignore some critical underlying demographic facts.

The current 63.5 percent American home-ownership rate combines two very different components: married households with about 78 percent home ownership, and not-married households with only 43 percent home ownership. Married households have a home-ownership rate 1.8 times higher — obviously a big difference. (As we have organized the data, these two categories comprise all households: “married” means married with spouses present or widowed; “Not-married” means never married, divorced, separated, or spouse absent.)

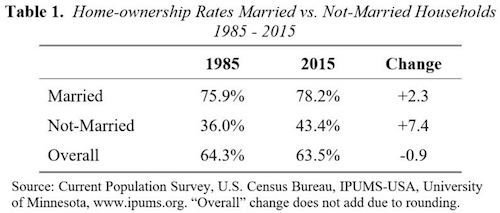

Table 1 contrasts home ownership by married vs. not-married households, showing how these home-ownership rates have changed since 1985.

One is immediately struck by a seeming paradox:

- The home-ownership rate for married households has gone up by 2.3 percentage points.

- The home-ownership rate for not-married households has gone up even more, by 7.4 percentage points.

- But the overall home-ownership rate has gone down.

How is this possible? The answer is that the overall home-ownership rate has fallen because the percentage of not-married households has dramatically increased over these three decades. Correspondingly, married households (which have a higher home-ownership rate) are now a smaller proportion of the total. Still, home ownership rose for both component parts. So the analysis of the two parts gives a truer picture of the underlying rising trend.

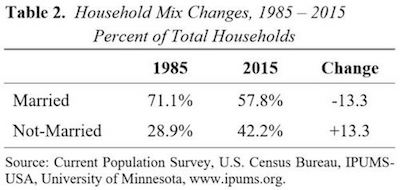

The dramatic shift in household mix is shown in Table 2.

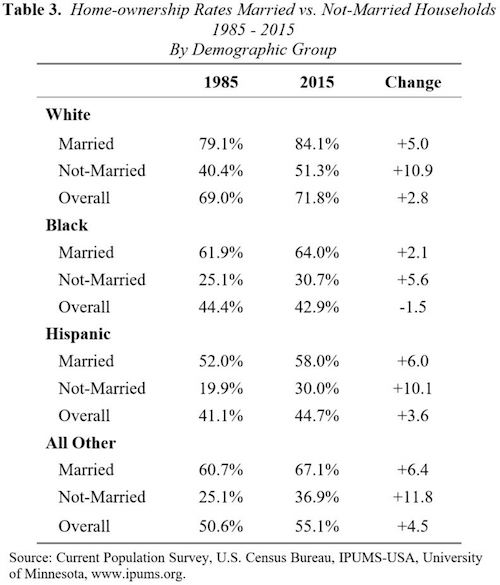

Table 3 shows that the strong contrast between married and not-married home-ownership rates and related changes from 1985-2015 hold for each demographic group we examined.

That is, home ownership for both married and not-married households went up significantly for all four demographic groups from 1985 to 2015.

Moreover, overall home ownership also increased for three of these four groups. Home ownership for black households, meanwhile, fell by 1.5 percentage points, though home ownership for both married and not-married components rose for this demographic as well. (This is consistent with that group’s showing the biggest shift from married to not-married households.)

In another seeming paradox, Hispanic home-ownership rates rose, while still contributing to a reduction in the overall U.S. rate. The reason for this is that their share of the population more than doubled, increasing the weight of their relatively high share of not-married households.

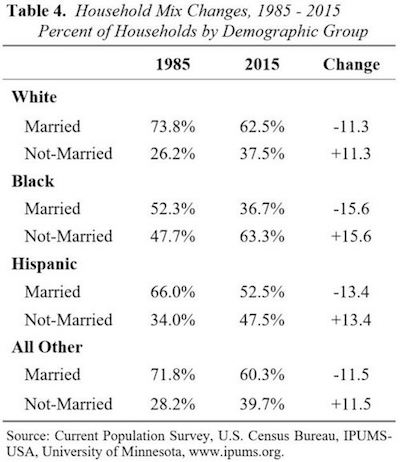

The trends by group in the mix of married vs. not-married households are shown in Table 4.

What would the U.S. home-ownership rate be if the proportions of married and not-married households were the same as in 1985? Applying the 2015 home-ownership rates for married and not-married households to the mix that existed in 1985 results in a pro forma U.S. home-ownership rate of 68.1 percent. This would be significantly greater than both the 1985 level of 64.3 percent and the 2015 measured level of 63.5 percent.

Adjusting for the changing mix of married vs. not-married households gives policymakers a better understanding of the underlying trends. This improved understanding is particularly important when weaker credit standards are being proposed as a government solution to the lower overall home-ownership rate.

To make sense of home-ownership rates, we have to consider changes in the mix of married vs. not-married households. And these changes have been dramatic over the last 30 years.

Alex J. Pollock is a distinguished senior fellow at the R Street Institute in Washington, DC. Jay Brinkmann is the retired Chief Economist of the Mortgage Bankers Association.